A number of these programs are readily available based upon buyers' earnings or monetary need. These programs, which generally use help in the type of deposit grants, can likewise save novice debtors substantial cash on closing costs. The U.S. Department of Housing and Urban Advancement lists newbie homebuyer programs by state.

All these loan programs (with the exception of newbie homebuyer support programs) are readily available to all homebuyers, whether it's your very first or 4th time acquiring a home. Many individuals wrongly believe FHA loans are offered just to newbie purchasers, but repeat borrowers can qualify as long as the buyer has not owned a main house for at least three years leading up to the purchase.

Mortgage lending institutions can assist analyze your financial resources to help determine the best loan products. They can also assist you much better comprehend the certification requirements, which tend to be complicated. An encouraging lending institution or home mortgage broker may also provide you homeworktargeted locations of your financial resources to improveto put you in the strongest position possible to get a home mortgage and purchase a home.

You're entitled to one totally free credit report from each of the 3 primary reporting bureaus each year through annualcreditreport.com. From there, you can spot and repair mistakes, deal with paying for financial obligation, and improve any history of late payments before you approach a home loan lender. It can be helpful to pursue financing prior to you get major about looking at homes and making deals.

Once you analyze your goals and figure out how much house your budget can manage, it's time to choose a home loan. With so numerous various home mortgages available, choosing one might seem overwhelming. Fortunately is that when you work with an accountable lender who can clearly discuss your choices, you can better pick a mortgage that's right for your monetary circumstance.

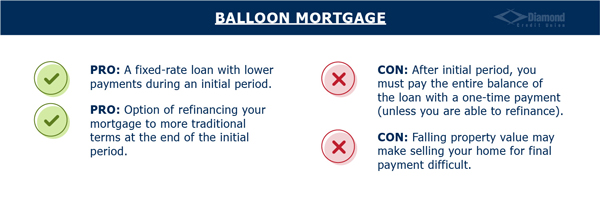

This provides you consistency that can assist make it easier for you to set a spending plan. what percent of people in the us have 15 year mortgages. If you prepare on owning your house for a long period of time (normally 7 years or more) If you think rate of interest could increase in the next few years and you want to keep the present rateIf you prefer the stability of a repaired principal and interest payment that does not changeAdjustable-rate mortgages (ARMs) have a rate of interest that may change occasionally depending upon modifications in a corresponding financial index that's associated with the loan.

ARM loans are generally named by the length of time the rates of interest stays fixed and how frequently the rate of interest is subject to modification afterwards. For instance, in a 5/1 ARM, the 5 represent a preliminary 5-year period during which the interest rate remains fixed while the 1 shows that the rate of interest is subject to modification when per year thereafter.

The smart Trick of What Are Brea Loans In Mortgages That Nobody is Talking About

These loans tend to enable a lower down payment and credit report when compared to conventional loans.FHA loans are government-insured loans that could be a good sirius xm cancel service fit for property buyers with limited income and funds for a down payment. Bank of America (an FHA-approved loan provider) uses these loans, which are guaranteed by the FHA.

To receive a VA loan, you need to be a present or former member of the U.S. armed forces or the existing or surviving spouse of one. If you meet these requirements, a VA loan could assist you get a mortgage. Lastly, make westlin financial certain to ask your lending specialist if they offer inexpensive loan products or take part in real estate programs used by the city, county or state real estate agency.

Find out about Bank of America's Budget-friendly Loan Option mortgage, which has competitive interest rates and offers a down payment as low as 3% (income limitations apply).

By Brandon Cornett 2020, all rights http://baldorc01o.nation2.com/what-percentage-of-mortgages-are-fha-for-beginners booked Copyright policy Editor's note: This short article was fully updated in March 2019 to bring you the current information (and resource links) regarding the different kinds of home loans that are available to borrowers. What are the various types of mortgage readily available to home purchasers in 2019, and what are the advantages and disadvantages of each? This is among the most common concerns we receive here at the House Purchasing Institute.

Follow the hyperlinks attended to even more details. And make sure to send us your concerns! If you currently understand the basic types of home mortgage, and you're ready to progress with the process, utilize one of the links supplied below. Otherwise, keep reading listed below to find out about the various financing alternatives available in 2019.

There are numerous different types of home mortgages offered to home purchasers. They are all thoroughly described on this website. However here, for the sake of simplicity, we have boiled everything down to the following options and classifications. As a debtor, among your very first choices is whether you desire a fixed-rate or an adjustable-rate mortgage loan.

Here's the main distinction between the two types: Fixed-rate home loan have the same rates of interest for the whole payment term. Because of this, the size of your monthly payment will stay the same, month after month, and year after year. It will never change. This is real even for long-lasting financing options, such as the 30-year fixed-rate loan.

The Basic Principles Of How Does Bank Know You Have Mutiple Fha Mortgages

Adjustable-rate home loan loans (ARMs) have an interest rate that will alter or "adjust" from time to time. Usually, the rate on an ARM will change every year after an initial duration of remaining fixed. It is for that reason described as a "hybrid" product. A hybrid ARM loan is one that begins off with a fixed or constant rate of interest, before switching over to an adjustable rate.

That's what the 5 and the 1 signify in the name. As you may envision, both of these kinds of mortgages have particular benefits and drawbacks associated with them. Use the link above for a side-by-side comparison of these pros and cons. Here they are in a nutshell: The ARM loan begins with a lower rate than the fixed kind of loan, however it has the unpredictability of modifications later on.

The primary benefit of a set loan is that the rate and regular monthly payments never ever change. However you will pay for that stability through greater interest charges, when compared to the initial rate of an ARM. So you'll need to select in between a fixed and adjustable-rate type of home loan, as discussed in the previous section.

You'll also have to choose whether you desire to use a government-insured home mortgage (such as FHA or VA), or a conventional "regular" kind of loan - mortgages what will that house cost. The distinctions in between these two mortgage types are covered below. A standard mortgage is one that is not insured or ensured by the federal government in any way.

Government-insured mortgage include the following: The Federal Housing Administration (FHA) home loan insurance program is managed by the Department of Housing and Urban Advancement (HUD), which is a department of the federal government. FHA loans are available to all kinds of borrowers, not just newbie buyers. The government insures the loan provider versus losses that may result from debtor default.